Racks & Retail: Why Amazon should be buying Britain's dead department stores

The high street is dying and the grid is full. Amazon is the one company that can vertically integrate to give life support to the UK’s high streets, whilst securing themselves prime commercial real-

There are two stories in British infrastructure right now that nobody seems to be telling together.

The first is that the high street is on its knees. The second is that the country physically cannot plug in the data centers it wants to build. On the face of it these are unrelated problems — one is a retail story, the other an energy one. But put them side by side and something interesting happens: each one looks suspiciously like the answer to the other.

And there’s exactly one company whose two halves slot neatly into the two halves of the problem. Amazon runs one of the largest cloud platforms on earth and one of the largest e-commerce and logistics operations in the country. Most operators eyeing this opportunity would have to pick a use for the building. Amazon doesn’t.

A sector in managed decline

By now, we’re all familiar with the state of British retail. According to the Centre for Retail Research, 2025 saw 17,349 store closures and just under 202,000 redundancies - and that came hot on the heels of a 2024 that saw roughly 13,600 stores shutter, getting on for 400,000 retail jobs gone in the space of two years. The British Retail Consortium has pointed out that there are now fewer people employed in UK retail than at almost any point on record.

The vacancy figures tell the same story from a different angle. National retail vacancy is hovering around the 12-14% mark, but that headline masks a brutal north-south split. London and Cambridge sit comfortably below 9%, while towns like Newport, Bradford and Blackpool are pushing close to one in five units standing empty. Online shopping now accounts for somewhere north of a quarter of all retail sales; a shift Amazon did more than anyone to drive. Meanwhile, footfall across high streets, shopping centres and retail parks remains stubbornly 15-20% below where it was pre-pandemic.

The point og this isn’t to wallow in the decline; we’ve all grown accustomed to the convenience of online shopping, and we’re very unlikely to return to traditional retail shopping in the same way we once did.

The point is that this has produced a very specific kind of asset: large, structurally-sound, well-located buildings that nobody particularly wants to use as shops anymore, available at a discount, in the middle of towns where people actually live and work.

Sound familiar?

It should - because it’s very nearly a shopping list for a modern data center site. It’s also, almost incidentally, a shopping list for a last-mile logistics node.

They need to be repurposed - so that the existing retail can remain, whilst the real monetisation comes from diversifying their uses.

The buildings fit the brief

Strip away the retail signage and look at what these buildings actually are, structurally and electrically, and the appeal becomes obvious.

1. They sit where the demand is. Department stores and large high-street units occupy prime, central positions inside developed urban areas. For latency-sensitive workloads - and increasingly that means AI inference served close to the end user, rather than bulk storage shoved out in a field - being in the city rather than 200 miles from it is the entire game. That same centrality is exactly what last-mile delivery economics are built on.

2. They already pull serious power. A former department store, supermarket or shopping centre was built to run escalators, full-building HVAC, commercial kitchens, refrigeration and lighting across tens of thousands of square feet. That means a substantial existing electrical supply with meaningful amperage already connected to the grid - an asset that, as I’ll come to, is now worth more than the building itself.

3. They’re multi-storey and built to last. These are semi-modern, structurally robust buildings with plenty of economic life left in the fabric. Multiple floors give you something a flat industrial shed doesn’t: vertical separation between functions, and a roof and basement that can be put to clever use.

4. They’re cheap. A distressed retail asset in a secondary location is changing hands at a fraction of its replacement cost. Compare that to the going rate for “powered land” - Savills has clocked sites with existing grid connections trading at £8-15m per acre, against £4.5-6m for ordinary London industrial land. The premium is entirely about the power, not the ground.

The elephant in the substation

Here’s the problem that makes all of this urgent rather than merely interesting.

You cannot get a grid connection in this country. The demand connection queue ballooned from around 41GW of contracted offers in late 2024 to 125GW by mid-2025 - for context, peak national electricity demand in February 2026 was about 45GW. Developers have reported waiting anywhere from five to ten years for a connection, with some quoted figures stretching far beyond that. More than three-quarters of UK data center developers are now actively looking at sites abroad rather than wait.

The grid needs a generational upgrade, and the uncomfortable truth is that there isn’t the public money to do it at anything like the speed required - a bottleneck I’ve written about before as the real anchor on data center progress, not the ability to stack servers in a building. NESO’s recent cull of the connection queue, slicing it from over 700GW down to a couple of hundred, tells you how much of the demand was speculative - but it also tells you how ferociously everyone is scrambling for the connections that do exist.

Which is exactly why an existing, energised building is such a quietly valuable thing. You’re not buying the shop. You’re buying the connection, and getting the building thrown in.

For Amazon specifically, this is the route around a queue that is otherwise throttling AWS’s ability to land new compute on UK soil - the very compute it needs for the AI and inference demand growing faster than anyone can build for. A distributed estate of modest, already-energised urban sites is a way to add capacity now, close to users, without betting everything on a single hyperscale campus that can’t switch on until the 2030s.

Engineering above and below the bottleneck

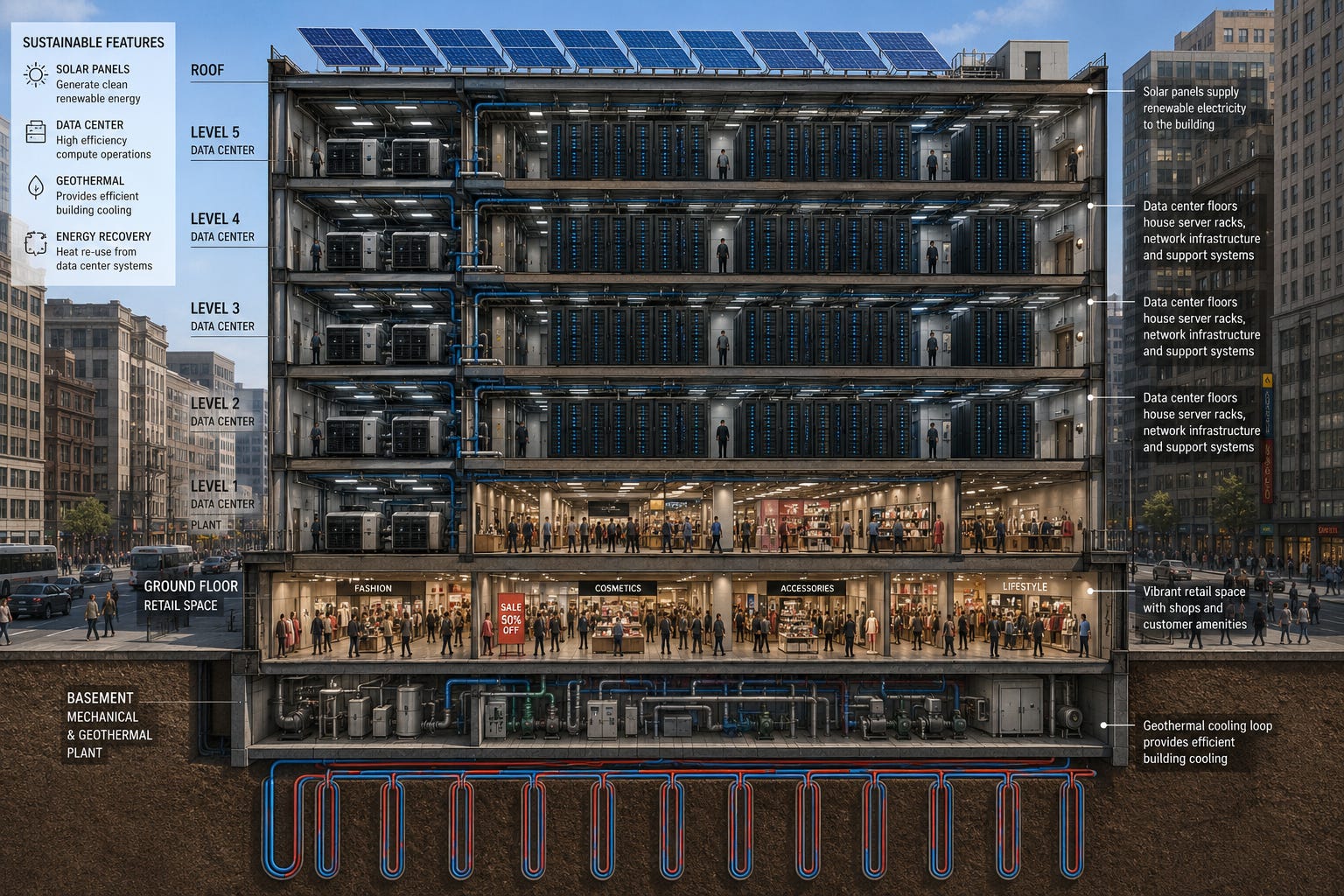

An existing supply gets you in the door, but an AI workload will want more than the building’s retail-era allocation. Rather than join the back of the decade-long connection queue, the smarter play is to generate and conserve as much as possible on-site - and a multi-storey building is unusually well set up for it.

Put the roof to work. A large, flat retail roof is prime real estate for solar PV; a private-wire array feeding the building directly, in the manner operators are already deploying to dodge grid delays.

Look down as well as up. The basement footprint sits right against the ground, making these buildings natural candidates for ground-source/geothermal exchange to shoulder the cooling load - which is where most of a data center’s parasitic energy goes in the first place.

Generate, store, and shave the peaks. On-site generation paired with battery storage turns the building from a passive load into something that can manage its own demand profile and lean on the grid connection only when it has to.

None of this gets you off the grid entirely, but it stretches a modest existing connection a great deal further. Crucially, it does so now, rather than in 2035.

The Amazon-shaped opportunity: compute upstairs, commerce downstairs

Here’s where this stops being a generic data center stategy, and becomes something only Amazon is really positioned to pull off. Simply gutting a high-street landmark and filling it with humming racks behind a blank façade would be a miserable outcome for everyone. The multi-storey layout lets you do something far more interesting - and Amazon happens to own both businesses that want the two halves of the building.

Upstairs: AWS, compute and AI. The upper floors become a compute node - energised, urban, low-latency. This is capacity for AWS’s cloud and the surging AI inference demand that increasingly needs to sit close to the people it serves rather than out in a remote campus. Each converted building becomes a small piece of a distributed edge network, plugged into AWS’s existing platform and operated by the team that already runs it. No competitor can integrate the racks into a live, global cloud with anything like the same low friction.

Downstairs: e-commerce and last-mile. The ground floor stays street-facing and working — but for Amazon, “retail space” means something specific. A central, well-connected unit is an almost perfect micro-fulfilment and last-mile delivery point: order online, dispatched from the heart of the town rather than a distribution park on the ring road; same-day collection lockers; returns drop-off; even a physical Amazon retail or Fresh footprint where it makes sense. The building feeds Amazon’s e-commerce machine from exactly the central location that makes last-mile economics work.

The elegance is that the two halves reinforce each other. The same building, the same energised connection, the same security and facilities team, the same logistics network that already moves Amazon’s goods can also move its hardware and spares. One acquisition, one operating model, two of Amazon’s core businesses fed at once. The compute makes the property pay; the fulfilment makes it pay twice.

And where a given site doesn’t suit either use, the ground floor still has civic value Amazon can bank as goodwill — reskilling and training centers for the post-AI labour market, in the very buildings that AI-era infrastructure now occupies, in the very towns that lost the retail jobs. For a company whose UK labour reputation is often heqavily scrutinized in the media, putting something genuinely useful back into those high streets is worth more than the floor space.

Even if Amazon doesn’t run it’s own retail space for it’s own enterprises, the operating model is the bit Amazon already understands: it runs and maintains the whole building, and where there are third-party ground-floor tenants, bills them through a service charge — the same arrangement any multi-let landlord uses, only here the landlord is running an AWS region upstairs and a fulfilment node downstairs.

A genuine win-win — if we keep it honest

Lay it all out and the alignment is almost too neat. Amazon gets prime, central, energised real estate at distressed-retail prices; sidesteps the worst of the connection queue; lands AWS and AI capacity close to users; and gives its e-commerce arm a last-mile footprint in the dead centre of town - all from a single class of cheap, overlooked building. The high street gets sustained private investment, a reason for footfall, and an anchor tenant with very deep pockets and no intention of leaving. And the town gets a community or skills asset funded by a commercial operator that’s still making a perfectly healthy return.

That’s the optimistic version, and I think it’s achievable. But I’ll end where I usually do on these ideas: this only works if it’s done in the open and within a competitive market. The very thing that makes Amazon perfect for this - that it already owns the cloud, the logistics and the retail brand - is also what should give us pause. There’s a version of this where one company quietly buys up the energised bones of the British high street and ends up owning both the compute and the commerce and the civic space of the places we live. National and community assets developed under a private umbrella are a fine thing right up until that umbrella becomes the only one in town.

Done well, the empty shop becomes the most useful building on the street again. We should just make sure it belongs to more than one landlord though; and so there’s as much opportunity for Oracle, Meta and Microsoft to deploy similar models also, although their benefits are not quite as clearly demarcated.

TH

You may also find these of interest:

Ctrl+Alt+Delete on Data Center Appraisal: A holistic asset algorithm that redefines conventional valuation methodologies

The more I've dug into the barebones of data center site deals, I've been left more confused than informed. Every deal is different. All can vary widely; with the valuation figures fluctuating wildly depending on:

The Proteus Protocol: How to rollout AI-ready data centers faster than your competitors for next-to-nothing

I'd forgive you if you'd never heard of Proteus before.

Tunnel Vision: A novel argument for a better subterranean data center design

Microsoft unveiled an ambitious project in 2015 - Project Natick. Simply put, the idea was to make an unmanned submarine full of servers, drop it into the sea just off the coast of California, and connect back to land via a big underwater cable.